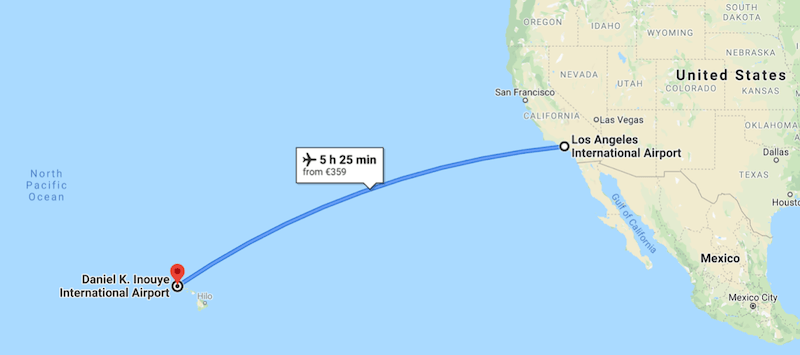

Imagine you are piloting an airliner from Los Angeles to Hawaii.

Little wiggle room for mishaps.

And you got 2’500 miles to fly.

25% of the distance (= 675 miles) into the trip, you want to know whether you are burning fuel efficiently and if you are going to make it to Daniel K. Inouye International Airport.

Just hoping that things are going to be alright is not a good strategy.

You want certainty for you and your crew.

So you grab a piece of paper to make a few calculations. The result:

You’ve flown 28% of the total distance, but you have used only 25% of the fuel.

This means you are well on your way! (assuming that for every mile flown, you are consuming about the same amount of fuel)

Had you used already 30% of the fuel supply, you’d have burnt too much and things might have gotten a bit dicey towards the landing.

Now that you know you are safe, you lean back in your seat and start dreaming about the waves in Waikiki Beach.

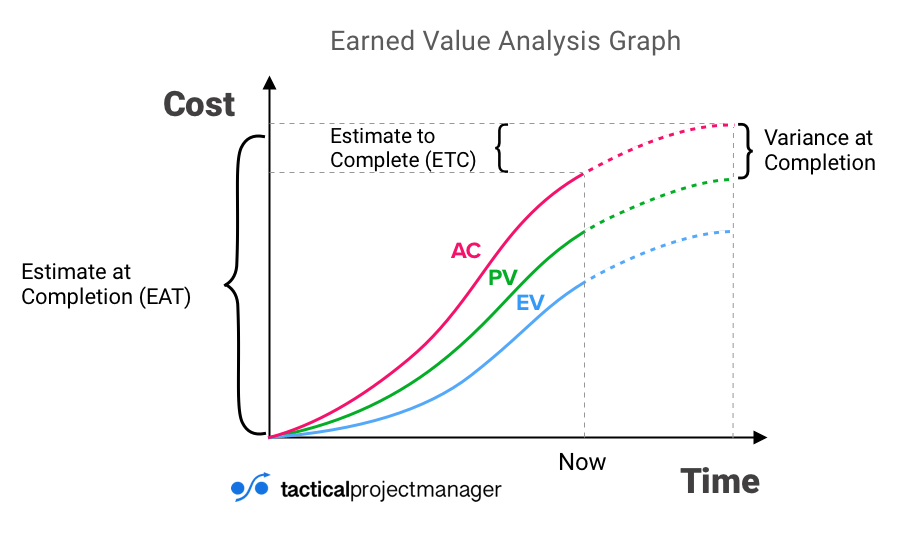

This story gives you an idea of the type of problem that Earned Value Analysis is used for.

EVA helps you assess whether you are on track in terms of budget and time.

Let’s transfer the example to the world of project management.

![]() Get my Earned Value Cheat Sheet! A PDF with all the definitions and formulas one sheet! Click there.

Get my Earned Value Cheat Sheet! A PDF with all the definitions and formulas one sheet! Click there.

![]() Are you looking for exercises to practice EVM formulas? Check out my new Earned Value Exercise Pack!

Are you looking for exercises to practice EVM formulas? Check out my new Earned Value Exercise Pack!

![]() Are you looking for exercises to practice EVM formulas? Check out my new Earned Value Exercise Pack!

Are you looking for exercises to practice EVM formulas? Check out my new Earned Value Exercise Pack!